Cost of Medicare Premiums: Planning can go a Long Way

Medicare is the federal government’s health insurance program for those over age 65 or for certain individuals who are disabled. There are four “parts”: Part A covers hospital expenses and is paid for by the government. Part C refers to Medicare Advantage plans offered by private insurance companies. Part B covers outpatient costs and equipment and Part D covers prescriptions; both B & D have premiums partially paid for by the Medicare recipient. The cost of the B & D premiums is means tested by way of your Adjusted Gross Income (AGI).

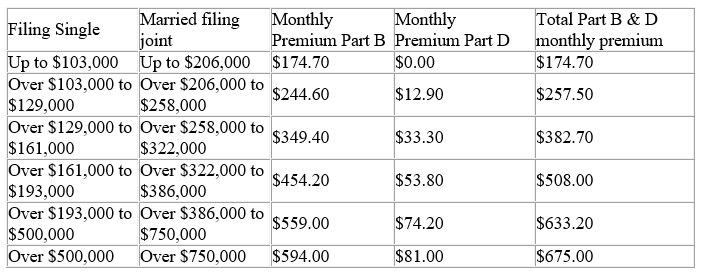

The base monthly premium in 2024 for Part B is $174.70. Social Security can tell you the exact amount you’ll pay for part B, as the “hold harmless rule” may apply to some (a topic for another day). Additionally, if you pay a late enrollment penalty, your amounts may be higher. Part D varies, averaging about $34.70. Depending upon your income, you may be subject to an “Income Related Monthly Adjustment Amount” (IRMAA) which is a surcharge added onto your premiums. In 2024 here is how is adds up according to your AGI.

The IRMAA Surcharge is determined by your AGI from the tax returns you’d filed two years previous. In other words, if you were a single filer in 2022 and had an AGI of $103,001, you’d pay the two monthly surcharges for your 2024 medicare premium. Therefore, it pays to be cognizant of your tax strategies beginning at age 63 as your AGI will apply to your Medicare premiums.

There are a number of factors that affect your AGI. For example, distributions that you take from your Individual Retirement Accounts (IRAs) count toward your AGI. Conversely, distributions taken from ROTH IRA’s do not count in your AGI. Conversions of IRA dollars to Roth IRA dollars count toward your AGI in the year of the conversion. Therefore, conversions prior to age 63 impact you more favorably in the light of keeping your Medicare premium surcharges down, versus after age 63. If you are already past age 63 and wish to consider conversions, consider spreading them out over a period of years, for example $20,000 per year for five years versus $100,000 all in a one year.

If you 63 or over, review your AGI when your tax returns are being prepared, before final submission to the IRS. There are a number of strategies to lower your AGI, particularly if you are just over a threshold. Speak with your tax professional regarding this, they will likely have some great suggestions for you.

LouAnn Schulfer of Schulfer & Associates, LLC Wealth Management can be reached at (715) 343-9600 or louann.schulfer@lpl.com. SchulferAndAssociates.com , louannschulfer.com or louann.biz

Securities and advisory services offered through LPL Financial, a Registered Investment Advisor. Member FINRA/SIPC.